VCs

What bear market? Investors throw record cash behind blockchain firms in 2021

VC investments into crypto over the first six months of 2021 have already more than doubled those witnessed in all previous years combined.

Despite the recent slight recovery of the cryptocurrency market, there is no denying the fact that the crypto industry has been faced with a great deal of volatility over the last few months, made evident by the total market capitalization of the sector that dipped from $2.5 trillion to $1.18 trillion over a 45-day span earlier this year.

Through all these ups and downs, however, 2021 has continued to see an increasing amount of capital enter this fast-evolving space. For example, reports indicate that over the first half of the year alone, venture capital (VC) funds poured in $17 billion into various crypto-related startups and companies.

To put things into perspective, the above-stated figure is by far the most witnessed in any single year and is nearly equal to the total amount raised in all previous years combined. Johnny Lyu, CEO of cryptocurrency exchange KuCoin, told Cointelegraph: “Early-stage investors of cryptocurrency have already achieved profitability and have a deep understanding of the development rules of the market. This is the key reason why they are willing to invest despite market fluctuations.”

Lyu further opined that for traditional investors, the crypto industry allows them to obtain higher returns in a shorter cycle, citing the volatility of Bitcoin (BTC) as an example of the same. “When the market experiences volatility, it is the best time for investing, and investors will profit from it.”

A closer look at the numbers

A hefty chunk of the aforementioned $17 billion figure comes from a single deal that saw a new cryptocurrency exchange called Bullish draw $10 billion in cash and digital assets following an initial injection by Block.one of $100 million, 164,000 BTC, and 20 million EOS tokens. Block.one led the capital raise alongside Peter Thiel, Alan Howard, Galaxy Digital and other investors.

In fact, just this one deal would have been enough to make 2021 the biggest year for venture capital investment in the crypto space, but if that wasn’t enough, the remaining $7.2 billion dollars would have equaled 2021 with 2018’s record of $7.4 billion raised, which is even more impressive considering that there are still five more months to go before the end of the year.

On the subject, Igneus Terrenus, head of communications for cryptocurrency exchange Bybit, told Cointelegraph that these numbers are not really startling since VCs are known for their voracious appetite for risk: “VCs are leveraging a relatively abundant and fungible resource — i.e., capita — to tap into something that is far scarcer and unique, which is partners and talents with whom they can build long-term value together.”

More notable VC activities

A little over a month ago, Silicon Valley-based venture capital firm Andreessen Horowitz announced the launch of its $2.2 billion crypto fund, with a spokesperson claiming that the company was “radically optimistic” about this space despite the price fluctuations. “We believe that the next wave of computing innovation will be driven by crypto,” partners Katie Haun and Chris Dixon were quoted as saying.

Furthermore, it should be pointed out that Andreessen’s first crypto-focused fund went live nearly three years ago, a time when the market was at its lowest levels historically, thereby showcasing the firm’s long-term belief in relation to this yet-nascent industry.

Similarly, Fireblocks, an infrastructure provider for digital assets, revealed that it had been successful in raising $310 million in a Series D round of funding, thus bringing the company’s total valuation to a whopping $2 billion in a period of less than six months. The fundraiser was co-led by institutional giants including Sequoia Capital, Stripes and the venture arm of Thailand’s oldest bank, Siam Commercial Bank.

Solana, a project that seeks to deliver a high level of scalability and transaction speed, also recently announced that it had completed a $314.15 million private token sale, making the nine-figure total the fourth largest fundraising event in the history of the crypto industry. Some of the company’s investors include Polychain Capital, Alameda Research and Blockchange Ventures, among others.

Cryptocurrency exchange FTX too recently closed a $900 million funding round, which saw a total of 60 participants, including Softbank, Sequoia Capital, Coinbase Ventures, Multicoin, VanEck and the Paul Tudor Jones family. As a result, the trading platform’s valuation has grown to $18 billion from $1.2 billion just a year ago, making it one of the largest cryptocurrency companies in the world.

Lastly, Dapper Labs, the team behind CryptoKitties and NBA Top Shot, secured about $305 million in new funding this March from a number of past and present NBA stars including the likes of Michael Jordan, Kevin Durant and Alex Caruso, and other investors including The Chernin Group and Will Smith’s venture capital outfit Dreamers VC. Following the closure of this latest funding round, Dapper Labs now reportedly holds a $2.6 billion valuation.

Is more institutional money incoming?

To gain a better understanding of whether more capital will continue to enter the crypto space, Cointelegraph reached out to Antoni Trenchev, managing partner at Nexo, a digital asset service provider. In his view, the crypto-finance sector possesses enormous untapped potential, especially with digital currencies allowing for an unprecedented level of inclusion for the under-banked. He added:

“The deals we are seeing right now — like Fireblocks snapping up $310M, SoftBank investing $200M in Brazilian crypto exchange Mercado Bitcoin — are being made by billion-dollar money managers after months of boardroom discussions and a result from long-term strategic decisions rather than momentary judgment.”

Not only that, fintech firms currently seem to have an unprecedented opportunity to build upon their existing client bases by offering modern products and services that users and companies really need, especially those that can serve as hedges against inflation — fears of which are looming large on the horizon all over the world.

Simon Kim, CEO at Hashed, an early-stage venture fund, believes that VCs are just now starting to understand the intrinsic value of crypto projects as it was difficult to justify the price of tokens that most blockchain projects had created in the past years:

“Ethereum is facilitating millions of transactions through numerous DeFi services, metaverse games and NFT services built on top of the network. There are now more than 20 million monthly active user accounts using Ethereum. The intrinsic value of DeFi tokens is even more apparent than Ethereum or Bitcoin.”

He further highlighted that much like how the IT industry leaders such as Amazon and Google grew amid the dot-com bubble, many crypto projects today have a solid foundation with a suitable business model and data. “This is why VCs are now pouring their money into crypto projects. They now believe that the next Google, Amazon and Facebook could be found in the space”, said Kim, closing out.

Related: COIN price fails to impress as more crypto firms are eager to go public

On a more technical note, Lyu highlighted that the increasing VC investments can, in large part, be attributed to the growing number of users that have seemingly flooded into various centralized exchanges (CEXs) and decentralized exchanges (DEXs) in recent months, adding: “Some popular DEXs such as Uniswap and PancakeSwap have exceeded traffic numbers related to some leading CEXs.”

What lies ahead?

Despite the COVID-19 pandemic that has had the global economy in a sort of standstill over the last year and a half, reports suggest that global venture capital funding over the first half of 2021 has shattered all previous records, with the figure now standing at $288 billion. That’s more than $100 billion when compared with the last six-month cycle record that was set during the second half of last year.

Jehan Chu, Managing Partner for Kenetic, a venture capital firm investing in blockchain companies, told Cointelegraph that the ongoing glut of capital sloshing around the world is forcing investors to take greater and greater risk in search of alpha, and despite ongoing institutional uncertainty about the future of crypto, they have no choice but to invest in the space:

“Fortunately, blockchain technology and crypto have graduated from a carnival freakshow to an inevitable future, so confidence in the underlying companies is at an all-time high. Additionally, a generation of cheap money flowing from the U.S. printing press has concentrated into the hands of investors. There has never been so much capital and the traditional gates have been eroded by partisan politics and poor financial management.”

Founding managing partner at Borderless Capital Arul Murugan believes that as more applications go live, greater infrastructure will be required to be built and as more infrastructure is built, it will attract even more applications, creating a virtuous cycle that started happening this year.

Not only that, he is of the opinion that the gap between traditional finance and decentralized finance (DeFi) is closing up with more people steering towards the crypto spectrum. Murugan opined: “Right now, crypto is less than 1% of traditional finance and people are seeing huge growth opportunities.”

Therefore, as an increasingly digitized future draws closer, the use of crypto tech will likely continue to grow, so it stands to reason that more players from the traditional finance space will continue to make their way into this burgeoning market, helping it to grow even further.

Funding Roundup: Derivatives and Defi Draw a Fresh Influx of VC Firms and Private Investors

As blockchain technology disrupts traditional industry standards, the list of progressive investors willing to stake their money has increased significantly. Leveraging this ongoing investment trend, both upcoming and ongoing projects are attracting millions of dollars from private investors, shaping a new era of decentralization. Globe DX Successfully Closes Fresh $18 Million Funding Round A new […]

As blockchain technology disrupts traditional industry standards, the list of progressive investors willing to stake their money has increased significantly. Leveraging this ongoing investment trend, both upcoming and ongoing projects are attracting millions of dollars from private investors, shaping a new era of decentralization. Globe DX Successfully Closes Fresh $18 Million Funding Round A new […]Uniswap v3 Is the Perfect Market Maker for Venture Capitalists

Uniswap’s key feature increases the gamification of the most popular DEX. But this is a game retail doesn’t have the tools to win.

Everyone’s a Market Maker on Uniswap

After announcements of announcements, the world was finally able to see Uniswap’s plans for its third version. Given that the project’s second version was one of the catalysts for DeFi’s meteoric rise in 2020, the anticipation for this release has been met with similar excitement. Indeed, Uniswap has regularly been at the forefront of innovation, especially for automated market makers (AMMs).

Automated market makers are the cornerstone of decentralized finance. To understand how revolutionary these are, one must first understand market-making functions in traditional finance.

Market makers offer assets at two prices, one for sellers and one for buyers. It profits from the spread between these two numbers. The real business of market makers is not price; it’s volume. The higher the volume, the higher the profit.

Due to the sheer amount of any singular asset needed, only institutions can be market makers in traditional finance. Even popular brokers like Robinhood rely on market makers to provide sufficient liquidity. This allows financial institutions to ever-so-slightly bend the rules of the game, if not directly change them for their own interests or those of their business partners.

Since January, this has been a highly debated topic when retail investors accused Robinhood and market makers of market manipulation.

Being the market maker confers undeniable advantages, and the invention of AMMs in DeFi has been a game-changer. Suddenly, everyone could be the market maker. Any liquidity provided to facilitate trades decreased the ask-bid spread, reduced slippage, and earned fees for the liquidity providers (LPs). The best part was that the liquidity pool is liquidity-agnostic; it doesn’t matter if one LP has invested millions in the pool or just a couple thousand dollars.

LPs are rewarded proportionally to their participation, but no one is excluded from market-making.

By automating the process of market-making, AMMs provided equitable opportunities to all market participants. With v3, however, this has changed dramatically.

Unpacking Concentrated Liquidity

One of the most impressive new features of Uniswap v3 is the possibility for LPs to provide liquidity within a specific price range. For example, while Alice provides liquidity to the entire DAI/USDC trading range, Bob can only provide liquidity to trades between 0.9-1.1DAI/USDC.

This means that Bob’s capital, as it is concentrated in just that range, will be more efficiently used in any trades between these two values.

In essence, if Alice and Bob have the same amount of capital but Bob concentrates his capital in a certain range around the current price, he will earn more in fees than Alice. The narrower the range at which Bob sets his liquidity, the more he will earn from fees than Alice as long as the price trades in that range. Alice’s strategy will shine if the price leaves that range as she will then earn all of the fees while Bob’s liquidity sits idle.

This also has a very positive effect on slippage, which effectively decreases as more capital is available around the current price rather than idle at both ends of the price curve. This decreases the price impact of any single transaction, so users effectively have a better rate than they would if there was less liquidity close to the current price.

1/

Uniswap v3 provides the only possible "solution" to impermanent loss and price impact

It also lets you reduce total price risk while increasing your impermanent loss (relative to v2) with concentrated liquidity

This might need a blogpost but I'll try a long thread first

— Hayden Adams 🦄 (@haydenzadams) March 24, 2021

Uniswap argues that in using concentrated liquidity, users can increase their capital efficiency by up to 4,000x when adding liquidity to a 0.10% price range, effectively increasing their fees while necessitating much less capital.

5/

💸 Concentrated Liquidity means LPs can earn the same amount of fees with just a fraction of the underlying capital, while keeping more of their total portfolio in desired assets!

🔥 Capital efficiency gains max out at 4000x for LPs adding liquidity to a 0.10% price range pic.twitter.com/aLUvBmbPGp

— Uniswap Labs 🦄 (@Uniswap) March 23, 2021

However, this is only true if all other actors keep providing liquidity to the entire price range. In reality, everyone will try to play the game of providing liquidity to a certain price range in the curve, with many strategies emerging to maximize fees.

What Uniswap hopes will happen is that different liquidity providers will choose different strategies.

Alice, for example, might concentrate all of her liquidity close to the current price, a highly crowded area but one in which most trades will happen, increasing her share of the pool’s fees.

Bob might provide his liquidity to the entire price range to receive fees on any single trade (albeit much fewer fees), which might pay off if the price is particularly volatile.

Max might think that the price of ETH/DAI will explode in the following days and concentrate all of his liquidity at a higher range. Max hopes that when the price arrives at this higher range, he will be in a prime position to earn more fees from trades in this less crowded range.

Applying Game Theory to v3

In reality, this is not how this will likely play out. To get a better understanding of the dynamics of liquidity provision in Uniswap’s v3, Crypto Briefing spoke with Nate Hindman and Mark Richardson from the Bancor team, one of Defi’s very first AMM projects.

“There is no advantage to being the early bird. As soon as the price moves, nothing is stopping other participants to change the price range at which they provide liquidity,” said Richardson.

In the above example, Max’s successful prediction of future price movement will not be rewarded. There is no reason to believe that actively managed liquidity will not be moved at the new price dynamically. Alice can easily and dynamically change the price range at which she’s providing liquidity and, as soon as the price reaches the range Max predicted, add her capital on top of Max’s and enjoy the same fees.

She could even provide it in a much narrower range than Max, effectively earning much more fees with a similar amount of capital.

“Uniswap v3 is brilliant, academically speaking,” adds Richardson.“But in practice, the laws of game theory predict that whales will compete to provide liquidity to the narrowest range possible around the current price and dynamically update their liquidity provision range to follow price.”

The only limit to how many times a day users could move their provision range is the gas fees necessary.

Imagine Alice and Bob are competing for the fees from the DAI/USDC pool. In v2, they would receive equal fees for equal capital in the pool. In v3, Alice decides she wants to provide her liquidity between 0.95-1.05 USDC/DAI. As most trades happen in that range, Alice immediately starts to receive more fees while Bob’s “wasted” capital on both extremities of the price range remains unused. Seeing his share of the fees go down, Bob decides to provide capital between 0.99-1.01 USDC/DAI.

In the case of a stablecoin pool, this range does not move, but in a pool between uncorrelated assets, things get trickier.

As soon as market players understand the new rules of Uniswap v3, everything changes. Institutions or larger whales will compete to provide capital in the narrowest range around the current price and use the fastest price oracles to update their positions every block. Smaller LPs would quickly fall behind as they are more hampered by gas prices and do not have the same access to formidable trading bots and price oracles.

This leads to what Richardson calls a race to the bottom. By setting a very small range for their liquidity, users effectively increase the risk of impermanent loss to hazardous levels.

When LPs provide liquidity to the ETH/DAI pair on Uniswap v2, they risk incurring impermanent loss on their stake. When the price of ETH decreases, they end up with more ETH and less DAI than they started with.

When the price of ETH rises, some of it is converted to DAI to keep a 50/50 split. Users may, in that case, make less on fees than they would have done had they just held their ETH. Users concentrating their liquidity to a very narrow range essentially enter a limit order.

If Alice provides liquidity to ETH/DAI in the 1,750-1,800 DAI/ETH range and the price of ETH moons, essentially all of her ETH will be sold to DAI at 1,800. If the ETH price continues to moon, too bad for Alice because she doesn’t hold any.

The other proposition is even more worrisome: Imagine Alice provides funds to the liquidity pool of a small DeFi project (called “RUG” for the sake of example) against ETH. She’s providing from 13-17 RUG/ETH. She began with 15 RUG and 1 ETH. But, hypothetically, a problem comes up in the development, which leads to a devaluation of the RUG token. As soon as the price of RUG drops below 13, Alice will be left only holding RUG. As Uniswap sells Alice’s ETH for RUG, the price continues to drop, causing chain liquidations of users’ concentrated liquidity positions.

Alice is soon left with a bag of worthless RUG and nothing else.

Entities handling huge amounts of capital may fare very well in Uniswap v3, but there may be hardly any rewards for retail investors trying to play the game.

The game favors whales, institutions, and investment funds with three key advantages at their service.

First, very high capital so that the fees associated with the constant on-chain movement of liquidity don’t represent too much of an investment. Second, swift price oracles can pinpoint exactly the price of an asset and the range it’s most likely to stay in until the next block of Ethereum is mined. Third, very advanced AI trading bots with human oversight to accurately predict the direction of price movement to best capture fees.

This is not a game humans alone can win.

Uniswap: VCs Favorite DeFi Exchange

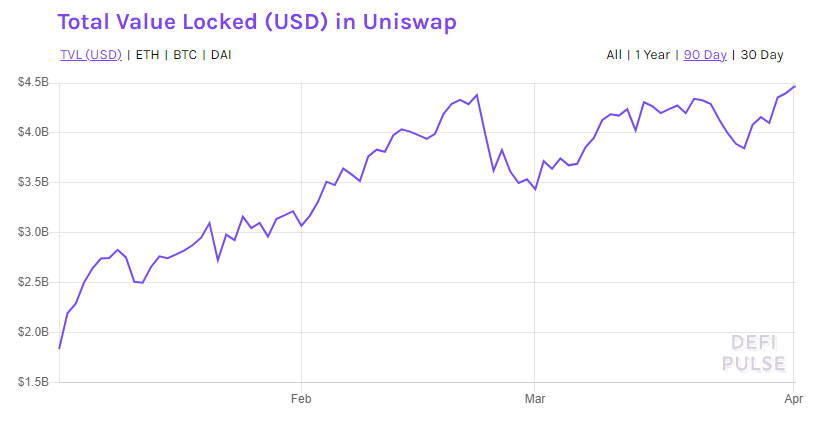

Uniswap is the flagship of DeFi. At the time of writing, the DEX has $4.41 million in Total Value Locked (TVL), according to DeFi Pulse. Its native token, UNI, enjoys a total market cap of more than $15 billion. The release of v3, however, didn’t include elements characteristic of DeFi releases, such as community involvement or voting on the proposed changes.

Uniswap treated the launch of v3 as reminiscent of Silicon Valley marketing tactics. Uniswap founder Hayden Adams relentlessly tweeted out clues, teasers, and announcements building massive hype ahead of the launch.

While this did bring a lot of attention to v3, it also showed how centralized the protocol’s governance had become.

The community was never involved in the making of v3. There was no opportunity for anyone to raise any legitimate concerns around the new system. Nor was there a vote among UNI token holders on whether to implement these changes.

Additionally, Uniswap announced no fees would be redistributed to UNI holders but that the fee switch could still, theoretically, be turned on at any moment. This fee switch would distribute part of the protocol’s fees to UNI token holders.

It’s also important to note that Uniswap received major investments from some of the biggest investors in Silicon Valley. Andreessen Horowitz was the lead investor in Uniswap’s Series A, but they’re certainly not the only ones: Union Square Ventures, Paradigm, and many others are all major stakeholders in Uniswap.

These investors represent a sizable part of all UNI tokens and, as such, hold the keys to the governance of one of the most valuable DeFi projects.

Balancing Efficiency and Community

If Uniswap were any Silicon Valley startup, judging v3 would be very different. The latest version of Uniswap is extremely capital efficient and, technically speaking, represents incredible innovations in the domain of AMMs.

But it raises an important question that DeFi would always eventually reach.

At what point does progress in the efficiency of protocols outweigh the importance of bottom-up governance, community building, and protecting regular users’ interests?

Uniswap’s v3 business license is the most obvious sign of this change in direction. While anyone can still see the code used by Uniswap, it is now protected by copyright for the next two years. Open-source code has been one reason behind the exponential growth of DeFi, but for Uniswap, this phase is over.

Uniswap Labs was asked for comments on Mar. 26. but has not yet responded to Crypto Briefing.

Disclosure: The author held ETH, DAI, BNT, and a number of other cryptocurrencies at the time of writing.