Did dYdX violate the law by changing their tokenomics?

The dYdX Foundation made an abrupt change to its project’s tokenomics, but it may have done so in consultation with its attorneys.

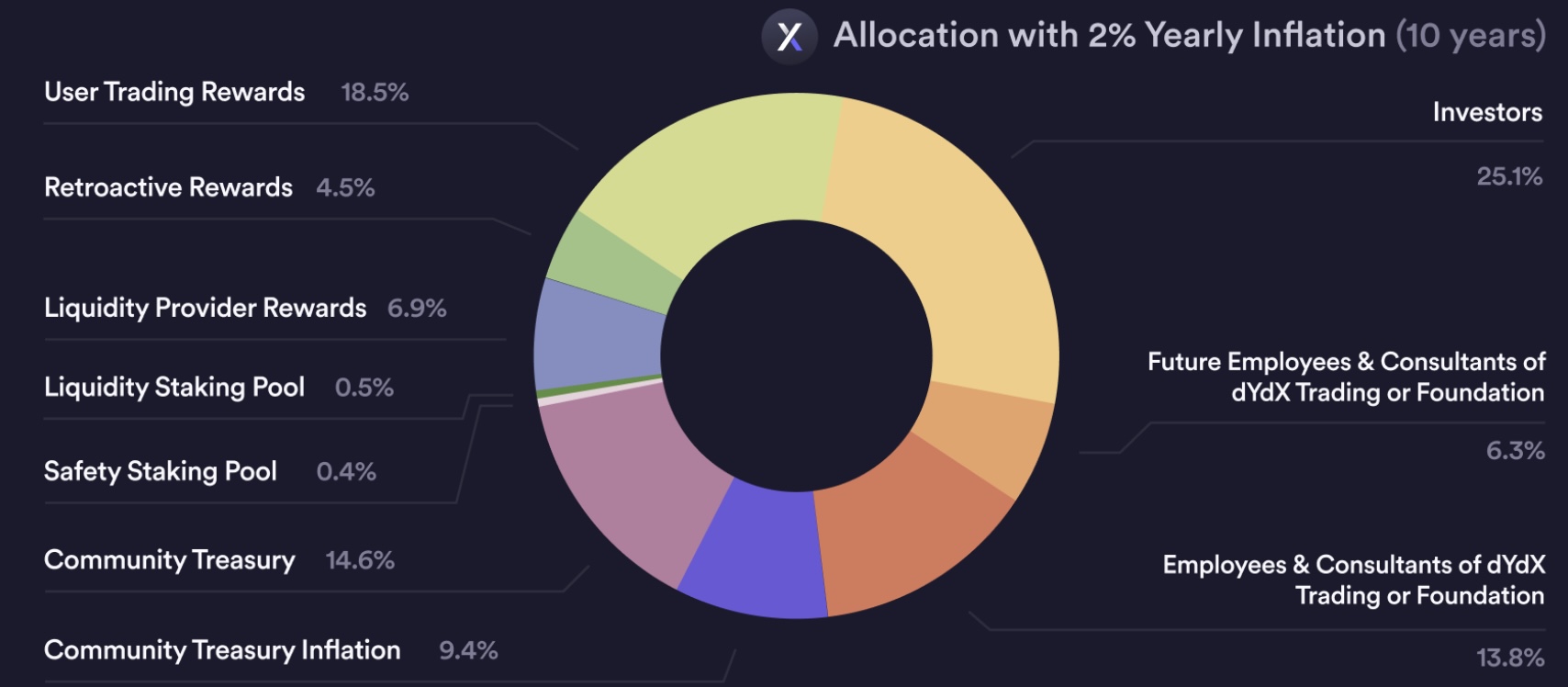

On Jan. 24, the dYdX Foundation, the entity responsible for the dYdX decentralized crypto exchange, announced “changes” to its tokenomics — the way it distributes tokens to early investors, employees and contractors, and, of course, the public.

So, what’s uncommon about the situation? The project’s foundation, in agreement with dYdX Trading Inc. and its early investors, decided to amend the project’s tokenomics and extend the period for which such investors’ initial batch of tokens would be locked, changing the date from Feb. 1 to Dec. 1, 2023. Whether this was a good or a bad thing depended on which side of the trade one was on. On the one hand, investors agreeing to hold their tokens for a longer period suggests a vote of confidence on their part in the project’s long-term success. On the other hand, anyone taking a short position in dYdX in anticipation of the increased supply might have been disappointed, as the token’s price rocketed following news of the amendment.

Related: My story of telling the SEC ‘I told you so’ on FTX

But why the delay? Although dYdX is not officially available in the United States, recent victories in enforcement actions on the part of the Securities and Exchange Commission may have prompted a heart-to-heart chat between the foundation and its attorneys. Now, whether the DYDX governance token might ultimately be viewed as a “security” under U.S. law could fill volumes and is outside the scope of this article. What matters is: Why would the signatories to the amendment to the lockup documents consent to a longer lockup? Why not let the tokens unlock and simply hodl them?

In the United States, all offers and sales of “securities” are either registered, exempt or illegal. Specific rules apply not only to the initial offer and sale of securities but also to resales — that is, sales by existing tokenholders to others. As a general matter, one may not serve as a conduit (legally speaking, an “underwriter”) between the issuer of the securities and the general public without following certain rules. Securities received in exempt offerings are referred to as “restricted securities,” and resales of the securities are an illegal “distribution” unless a safe harbor applies.

One such safe harbor is Securities Act Rule 144. One must follow the restrictions of Rule 144 in order to qualify for relief and sell without fear of being deemed an “underwriter.” There are classes of restrictions that apply to different types of holders — specifically, “affiliates” (those who control or are controlled by the issuer) and “non-affiliates.” All sales, affiliate or non-affiliate, are subject to a one-year holding period. This holding period establishes, in theory, that the securities were purchased with “investment intent,” not for immediate dumping on the unsuspecting public.

Sales by affiliates are subject to other restrictions, including that there is “current public information” available about the issuer, limitations on how many securities can be sold in a given period of time, manner of sale restrictions and filing requirements.

Related: Crypto users push back against dYdX promotion requiring face scan

While it is highly unlikely that dYdX insiders long to be subject to the full gamut of United States securities law, perhaps they were inspired by its basic principles, especially if they have short holding periods in the tokens. A common vehicle used by crypto projects to attract early-stage capital, for example, is a “simple agreement for future tokens,” or SAFT. This type of agreement does not convey the tokens immediately but promises to do so in exchange for an up-front investment. As noted above, if you are subject to a holding period on your restricted securities, you must own them in the first place to start the clock running. It is unclear whether the foundation used SAFTs for its investors, but if it did, some of the investors might be new to ownership indeed.

Maybe the dYdX investors who participated in the decision to change its tokenomics wanted to signal their confidence to the market by delaying their access to the tokens. It’s possible they anticipated the pump that followed news of the amendment. Or, perhaps they were inspired by U.S. laws and are looking to inch toward eventual compliance with those laws. It will be interesting to see what other measures, if any, dYdX takes with respect to token emissions going forwar.

This article is for general information purposes and is not intended to be and should not be taken as legal or investment advice. The views, thoughts, and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.

Go to Source

Author: Ari Good