How to earn passive income with peer-to-peer lending

P2P lending is a way for individuals to lend money directly to other individuals without involving traditional financial institutions, such as banks.

What is peer-to-peer (P2P) lending?

Peer-to-peer (P2P) lending, also referred to as marketplace lending, is a type of lending that uses online platforms to link lenders and borrowers directly, eliminating the use of conventional financial intermediaries, such as banks.

In P2P lending, individuals or businesses seeking loans can request funding by creating loan listings on a P2P platform. Individual investors or institutional lenders, on the other hand, can analyze these listings and decide to fund them based on their level of risk tolerance and expected rate of return.

P2P lending platforms serve as intermediaries, enabling the loan application, credit evaluation and loan servicing processes. They leverage technology to improve the user experience and pair lenders and borrowers. The loans may be used for a variety of things, including debt consolidation, small company loans, school loans and personal loans.

P2P lending platforms function within the legal restrictions imposed by the country in which they are based. Platforms must abide by all applicable laws, particularly those relating to borrower and investor protection, which differ depending on the country’s regulations.

Examples of P2P lending platforms

LendingClub is one of the largest P2P lending platforms in the United States. It offers personal loans, business loans and auto refinancing options. Zopa is another prominent P2P lending platform in the United Kingdom. It offers personal loans and investments, connecting borrowers and investors directly.

Aave is a decentralized P2P lending platform on the Ethereum blockchain that enables users to lend and borrow cryptocurrencies at interest rates that are based on supply and demand dynamics. It provides a wide range of features, including incentives for liquidity mining, flash loans and collateralized borrowing.

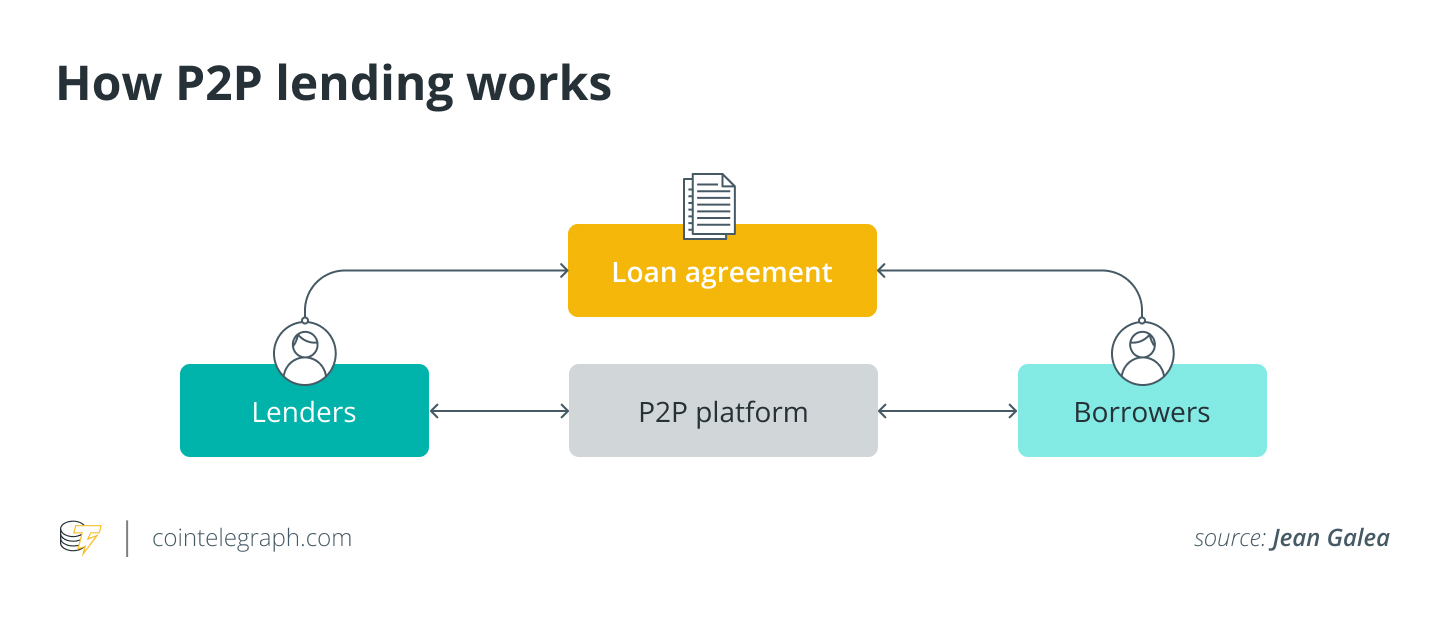

How does P2P lending work?

Let’s understand the P2P lending process using an example. Say Bob wants to borrow $10,000 to consolidate his debt. On a P2P lending platform, he submits a loan application and includes his financial details and loan justification. After evaluating John’s creditworthiness, the platform lists his loan.

A platform user named Alice reads John’s loan listing and decides to fund $1,000 of the loan because she thinks it fits with her investment philosophy. As additional lenders follow suit, Bob receives the $10,000 when the loan has been fully funded. The P2P lending network disperses Bob’s monthly repayments, which include principal and interest, among the lenders over time. Bob pays interest, which gives Alice and other lenders a return on their investment.

The step-by-step process of P2P pending between Bob and Alice is explained below:

- Bob submits an application for a $10,000 loan for debt consolidation on a P2P lending website.

- Based on Bob’s financial information and loan purpose, the P2P lending platform evaluates his creditworthiness.

- The platform lists Bob’s loan request along with information about the amount, annual percentage rate and purpose of the loan.

- Following an examination of the various loan listings, Alice, a platform investor, chooses to contribute $1,000 to Bob’s loan.

- Bob receives the $10,000 loan amount after additional lenders have fully funded the loan.

- Bob pays the P2P lending platform a certain amount each month in principal and interest.

- The P2P lending network collects Bob’s repayments and then distributes them to other lenders, such as Alice.

- Through the interest payments made by Bob over time, Alice and the other lenders make money on their investments.

Related: What is P2P trading, and how does it work on peer-to-peer crypto exchanges?

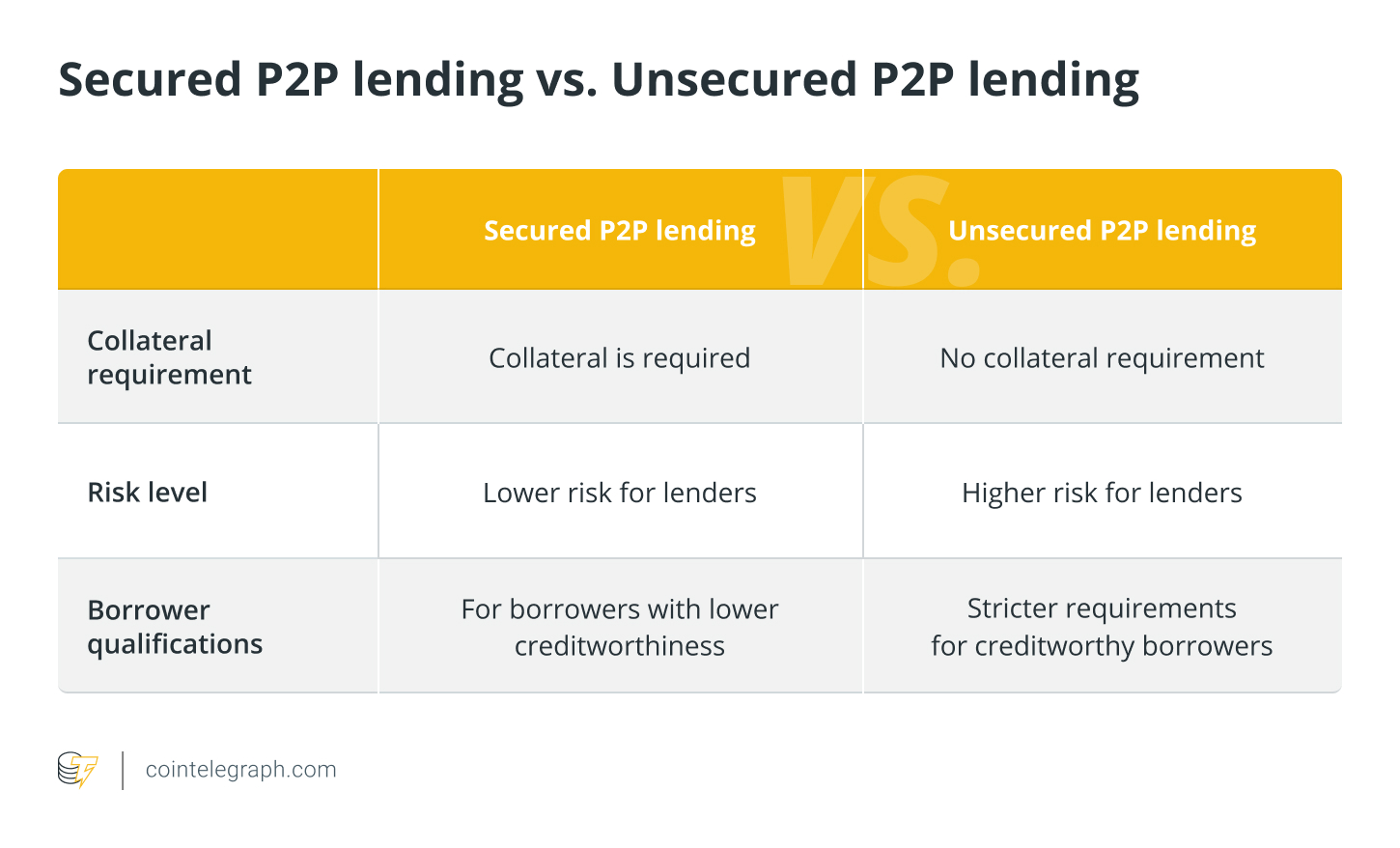

Secured vs. unsecured P2P lending

Secured and unsecured P2P lending are two distinct approaches to lending in the context of peer-to-peer platforms. Secured P2P lending refers to loans backed by assets, such as traditional ones like real estate or cars, as well as digital ones like cryptocurrency, as collateral. When a borrower defaults, the lender can seize and sell the collateral to recover their funds.

On the other hand, unsecured P2P lending does not require collateral. Lenders base their risk evaluation on the borrower’s creditworthiness and financial background. In cases of default, lenders often turn to legal procedures for debt recovery as they have no specific assets to seize in the event of a default.

The P2P platform’s collateral policies, interest rates and risks must be carefully considered by both borrowers and lenders when considering offering an unsecured loan.

How to become a peer-to-peer lender

Find a P2P lending platform that fits your investment preferences before applying to become a peer-to-peer lender. Choose platforms with a solid reputation, clear pricing arrangements and a history of effective loan transactions. Additionally, users should become familiar with the P2P lending regulations in their country since there may be certain requirements or licensing procedures to follow.

Create an account by entering the required information, such as identification verification and banking information, after selecting a platform. Next, deposit the money users want to use to invest in P2P lending into their accounts. This sum will act as their capital for lending.

Users will have access to loan listings on the site as P2P lenders. These listings provide information on the borrowers, the goals of the loans, the interest rates and the risk levels. Based on their investment criteria and risk tolerance, users should evaluate each listing.

After deciding which loans to sponsor, users should keep a tight eye on their holdings. They should keep track of the due dates, interest accruals and any late payments or defaults. Some platforms offer automated reinvestment options that allow users to put repayments toward new loans to raise their potential profits.

However, as there are risks involved with peer-to-peer lending, such as the potential for borrower defaults, investors should carefully analyze borrower profiles and loan details before making lending decisions.

Can you make passive income by investing in P2P lending?

P2P lending can provide passive income to lenders, as discussed below:

Regular interest income

P2P lenders can earn recurring interest on their loans. Borrowers’ interest payments generate money during the loan period. This income can be a source of passive cash flow, especially if investors have a diversified portfolio of loans.

However, the amount of interest earned depends on the loan amount, the interest rate and the borrower’s repayment behavior.

Passive portfolio management

P2P lending systems manage loan servicing, payment collection and lender distribution once lenders select and fund loans. Passive portfolio management lets them earn without actively managing loans.

The platform makes sure that lenders receive their fair share of interest payments and that borrower repayments are completed.

Automated investment

P2P lending platforms offer automated features and tools to simplify investing. Auto-invest options automatically distribute funds to new loans based on lenders’ predefined criteria, eliminating manual selection and investment decisions.

Reinvest repayments

As borrowers repay their loans, lenders can expand their total loan portfolio and raise interest income by continuously reinvesting the repayments. Reinvestment allows lenders to compound their earnings and potentially grow their passive income over time.

Risks and rewards of investing in P2P lending

Investing in P2P lending comes with both risks and rewards, as explained in the sections below:

Risks associated with P2P lending

- Default risk: P2P lending is risky due to borrower defaults. Borrowers may default, losing principle and interest income.

- Credit risk: P2P lenders lend to individuals and small businesses of varying creditworthiness. Therefore, borrowers with high-risk exposure may default.

- Lack of collateral: Lenders may have few assets to recover in the event of a default, raising risk.

- Platform risk: Lenders may face trouble getting their money back if a P2P platform encounters operational problems, financial instability or fails altogether.

- Market and economic risk: Financial instability and economic downturns can increase default rates and decrease the value of loans in the secondary market.

Rewards offered by P2P lending

- Higher returns: P2P lending can outperform fixed-income investments. Investors can outperform savings accounts and other low-yield assets by lending directly to borrowers.

- Diversification: P2P lending lets investors diversify across multiple loans, reducing portfolio risk and loan defaults.

- Passive income: Monthly or quarterly interest payments make P2P lending a passive revenue source. Investors can benefit without actively managing their holdings.

- Access to credit market: P2P lending networks offer financing to borrowers who may not qualify for bank loans, which helps promote financial inclusion and may yield high rewards for lenders.

- Transparency and control: Investors can check borrower profiles, loan information and hazards on P2P lending platforms and choose loans that match their risk tolerance and investment criteria.

Therefore, before engaging in P2P lending, it’s critical for both lenders and borrowers to carefully consider and comprehend the risks involved. Some of the tactics that can help reduce these risks include diversification, caution and choosing reliable platforms.

Collect this article as an NFT to preserve this moment in history and show your support for independent journalism in the crypto space.

Go to Source

Author: Jagjit Singh