Crypto P2P scams in India show digital asset education is needed

Scammers have made it impossible for Indian crypto traders to conduct P2P trades owing to several police complaints and bank account freezes that follow.

Peer-to-peer (P2P) cryptocurrency trading has been a staple of the cryptocurrency community since the industry’s early days.

P2P trading refers to the direct exchange of cryptocurrencies between two users without the involvement of intermediaries. P2P exchanges link buyers and sellers while also adding an extra degree of security through an escrow service. Some of the key advantages of P2P over centralized exchanges include global accessibility, a variety of payment alternatives and no transaction fees.

Furthermore, P2P marketplaces have become crucial for crypto traders and enthusiasts in jurisdictions where governments are hostile to formal cryptocurrency exchanges and service providers.

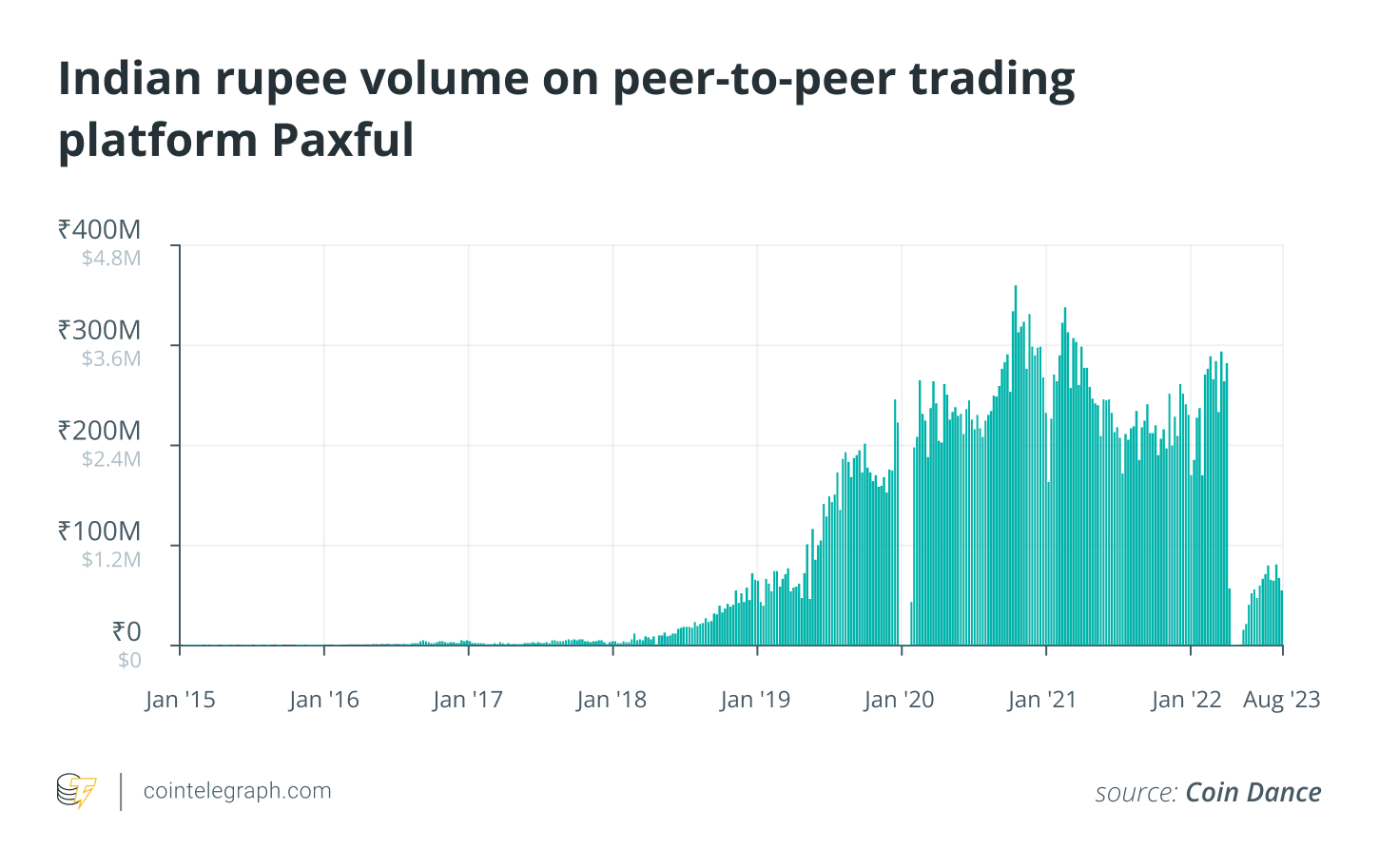

In India, they became a lifeline for many crypto traders when the country’s central bank issued a banking ban on cryptocurrency businesses in April 2018.

Although the banking ban was eventually lifted by the Supreme Court in March 2020, P2P platforms continue to play a crucial role as banks remain sceptical about offering services to crypto exchanges due to a lack of regulatory clarity.

During the bull market in 2021–2022, India saw a significant surge in crypto trading volumes and crypto platforms, prompting the government to take notice of the nascent ecosystem.

Recent: PayPal’s new PYUSD stablecoin faces legal headwinds and ‘less functionality’

While industry leaders demanded a comprehensive regulatory framework, which has been under development since 2019, the Indian finance minister announced a 30% tax on crypto profits in 2022.

The heavy tax, in addition to the continuing lack of regulatory clarity, has been the bane of the budding Indian crypto ecosystem, deterring Indian investors away from the market.

While mainstream crypto exchanges struggled, P2P platforms saw their volumes skyrocket.

How P2P scams happen

This rise in P2P trading volume also led to significant uptick in P2P scams. These scams often use stolen banking data or lure customers with fake promises of high profits and then use their banking information to scam P2P users.

Earlier in July, two people were arrested in the Indian city of Ujjain in connection with a Binance P2P scandal. The police recovered several fake bank accounts, ATM cards and documents from the accused, who were allegedly buying fake IDs and personal data for 1,500 Indian rupees ($18) in order to scam users of Binance P2P.

Two Accused In Binance P2P Scam Arrested In Ujjain, India

Two accused of scamming people on #Binance P2P arrested by police in Ujjain, India. Many fake bank accounts, ATM cards and documents are seized from accused

The accused used to buy Fake ID Proofs and personal data… pic.twitter.com/Nt5GxhVmio

— Ajay Kashyap (@EverythingAjay) July 11, 2023

One way P2P scammers steal user data is with the help of fake crypto-centered channels on Telegram that promise high profits or airdrops. Many gullible users looking to make a quick profit often join these channels and share their personal banking information. In many other cases, the scammer simply buys or steals the user’s personal information.

The stolen data is then used to create a P2P account on any popular P2P platform — Binance and WazriX are common in India.

The scammer then initiates a buy order on the P2P platform looking for unsuspecting sellers. Once they match with a seller, they send the money to the seller using the victim’s account. Thus, they complete the P2P transaction on the platfrom where the buyer receives the cryptocurrency and the seller receives the money in their bank account.

The buyer (scammer) then vanishes with the crypto and the victim whose bank account was used to send the money only realizes it after the money has been deducted from their bank account.

The victim then lodges a complaint with the police whose first step is to freeze all bank accounts that the victim has interacted with during the scam phase.

This action from the police triggers an extended account freeze for unsuspected sellers of the P2P platform who only realize they were involved in the scam after they get a call from the police or their bank informs them that their account has been frozen.

In one instance, a seller, who wished to remain anonymous, received a “bank account frozen” message while trying to pay for a taxi. After contacting the bank, the seller learned that the halt was requested by the police’s cyber division responsible for looking into online crimes.

When the seller then followed up on the complaint with the police and enquired about the freeze on the account, they were met with threats of legal consequences from the Enforcement Directorate, India’s economic intelligence agency, for a $40 P2P completed transaction on WazirX in October 2022.

The police complaint was filed by a woman who was scammed out of $30,000 between September 2022 and June 2023. The police started the investigation and froze every bank account that interacted with the plaintiff’s accounts during the mentioned time frame, including the sellers for the October transaction.

The seller tried to explain to the police officer that they had successfully completed the P2P transaction and thus have no role in the scam. Despite this, the police ignored their claims, erroneously claiming that crypto transactions are illegal and stating that they must pay the complainee $40 or face further legal action.

With no other options left, the victim eventually paid the $40 amount to the plaintiff’s account after which the police released an order to unfreeze the account.

The police did not respond to Cointelegraph’s request for comment.

The bank account restrictions limit unsuspected victim’s access to cash, and the complexities involved in getting the issue fixed are significant. The seller — who often is also unaware of the scam until the last moment — could be subject to a legal investigation or be required to provide evidence.

Problem using P2P in India still continues. @cz_binance do something. @TheOfficialSBI Got my account frozen. pic.twitter.com/Y6By4l5RGy

— Balamurugan Lakshmanan (@balamurugankl) July 11, 2023

There have been several instances of such P2P scams over the past year where victims noted their fear of authorities, with police often threatening legal actions. The anonymous seller told Cointelegraph that their account was frozen with 50,000 rupees in it, adding that they are very afraid of how to approach authorities and whether they would face legal consequences.

Some advise against P2Ps

Due to a lack of clear guidelines around crypto-related crimes and a lack of understanding of the technology underpinning cryptocurrencies, police investigations often start with freezing the accounts of anyone involved in the situation.

Pushpendra Singh, a prominent crypto personality and educator in the Indian crypto ecosystem, told Cointelegraph that scammers take advantage of the police’s ignorance of how crypto works:

“What these scammers do is they often use platforms, such as international Binance platform, to evade investigation from the Indian authorities, as it becomes quite difficult for the authorities to demand documents from such international platforms. Scammers then take the stolen USDT to Trust Wallet or any other non-KYC’d platform to avoid being tracked. While scammers get away with the money, both buyer and seller in the transaction face financial and legal consequences.”

Singh said that Indian police need to be actively trained on how these scams work. He noted that the “lack of awareness around the nascent tech also leads to victim harassment where many victims are often told by the police that crypto transactions are illegal in India.”

P2P scams have become very common and concerning to the point where the majority of crypto experts in India have now asked traders to avoid P2P trading. Sumit Gupta, CEO of CoinDCX — a major crypto exchange in India — said crypto traders should avoid P2P transations.

Magazine: Should we ban ransomware payments? It’s an attractive but dangerous idea

He said that many people in India got a notice from various government authorities just because they unknowingly sent money from someone who wasn’t the right person to deal with.

Guys, P2P is extremely risky. I’ve been telling folks to avoid using any kind of P2P platforms, it’s an open invitation to trouble.

I know so many people in India got notice from various govt authorities just because they unknowingly sent INR or received INR from someone who… https://t.co/3CoyceiPwP

— Sumit Gupta (CoinDCX) (@smtgpt) April 28, 2023

Other crypto personalities have urged traders to be vigilant and make sure the P2P account one is interacting with has a good history.

What started out as a crypto revolution has turned into a weak spot for the Indian crypto ecosystem.

Collect this article as an NFT to preserve this moment in history and show your support for independent journalism in the crypto space.

Go to Source

Author: Prashant Jha